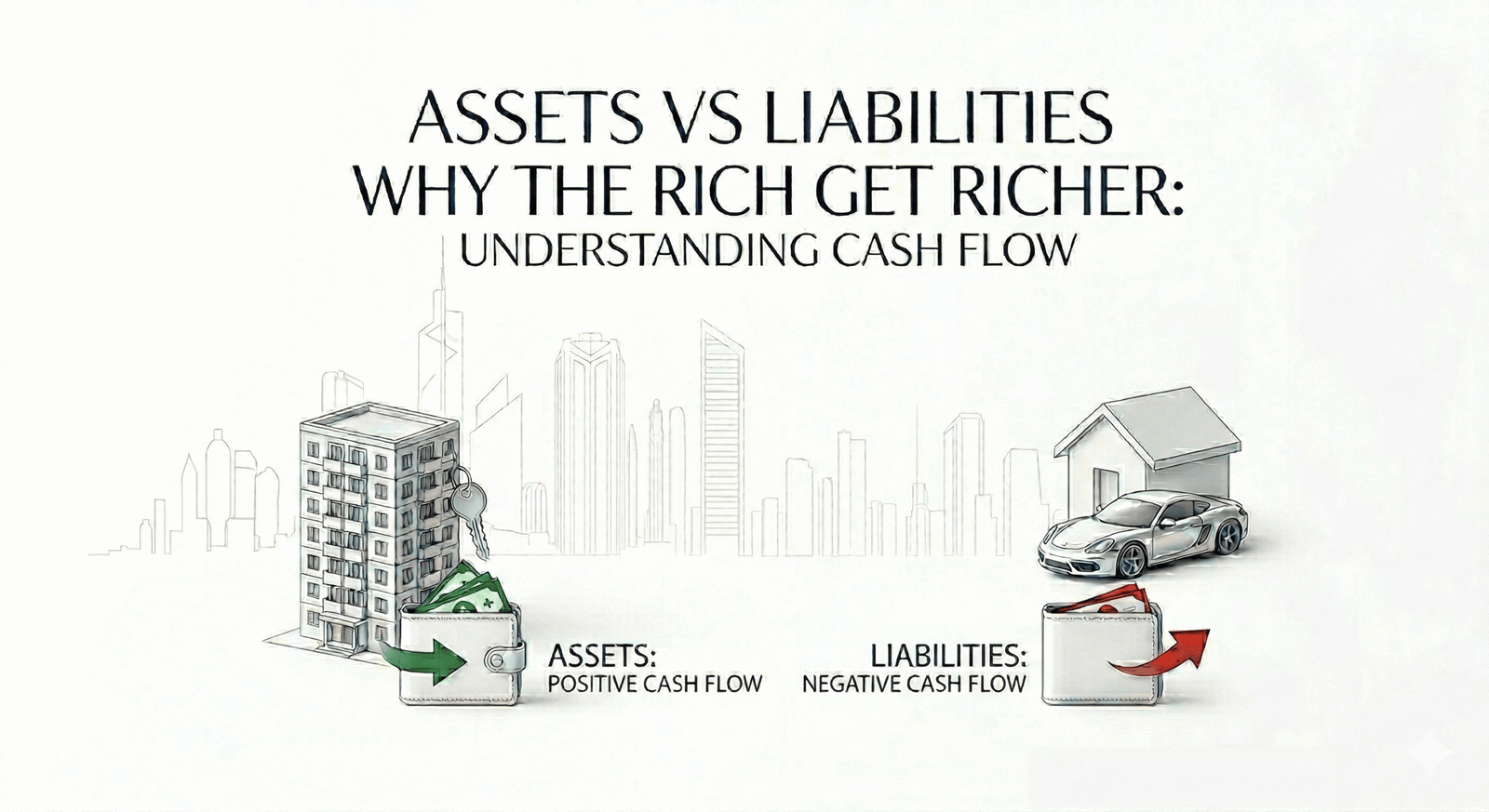

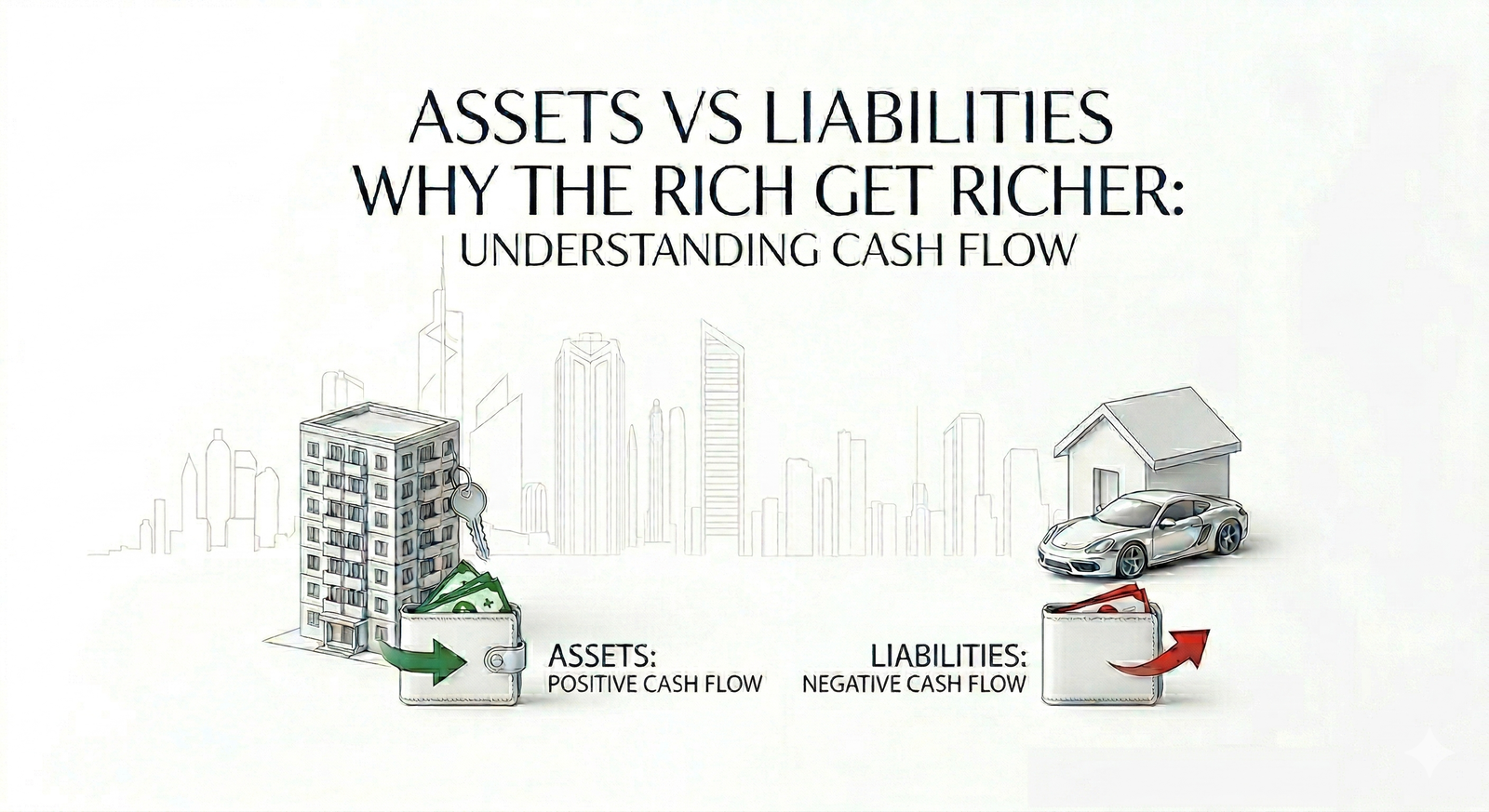

Assets vs Liabilities: Why the Rich Keep Getting Richer

Most people spend their lives working for money. The wealthy focus on building systems that make money work for them. That difference may sound simple, but it changes everything. One of the most powerful financial lessons behind long term wealth is understanding assets vs liabilities. Robert Kiyosaki popularized this idea by defining an asset as something that puts money in your pocket and a liability as something that takes money out. That cash flow based framing became one of the central ideas of the Rich Dad philosophy.

This idea matters because many people think they are buying assets when in reality they are buying obligations. Something may look valuable. Something may impress other people. Something may even rise in price over time. But if it keeps demanding money from you and gives nothing back in regular income, then from a practical investor’s point of view, it behaves more like a liability than a wealth building asset. That is exactly why the assets vs liabilities concept remains so powerful in personal finance and real estate education.

At IMLAAK, this is one of the most important ideas we believe investors should understand clearly, because wealth is not built by appearance. Wealth is built by cash flow, discipline, and repeated allocation into productive assets.

“Do not buy things that look rich. Buy things that build cash flow.”

What Robert Kiyosaki Really Meant by Assets vs Liabilities

Robert Kiyosaki’s definition became famous because it cut through traditional financial jargon and focused on real life outcomes. His philosophy asks a simple question: does this put money in your pocket, or does it take money out of your pocket? Rich Dad’s official philosophy page still frames the concept that way, and related articles continue to emphasize that the practical test is cash flow, not image.

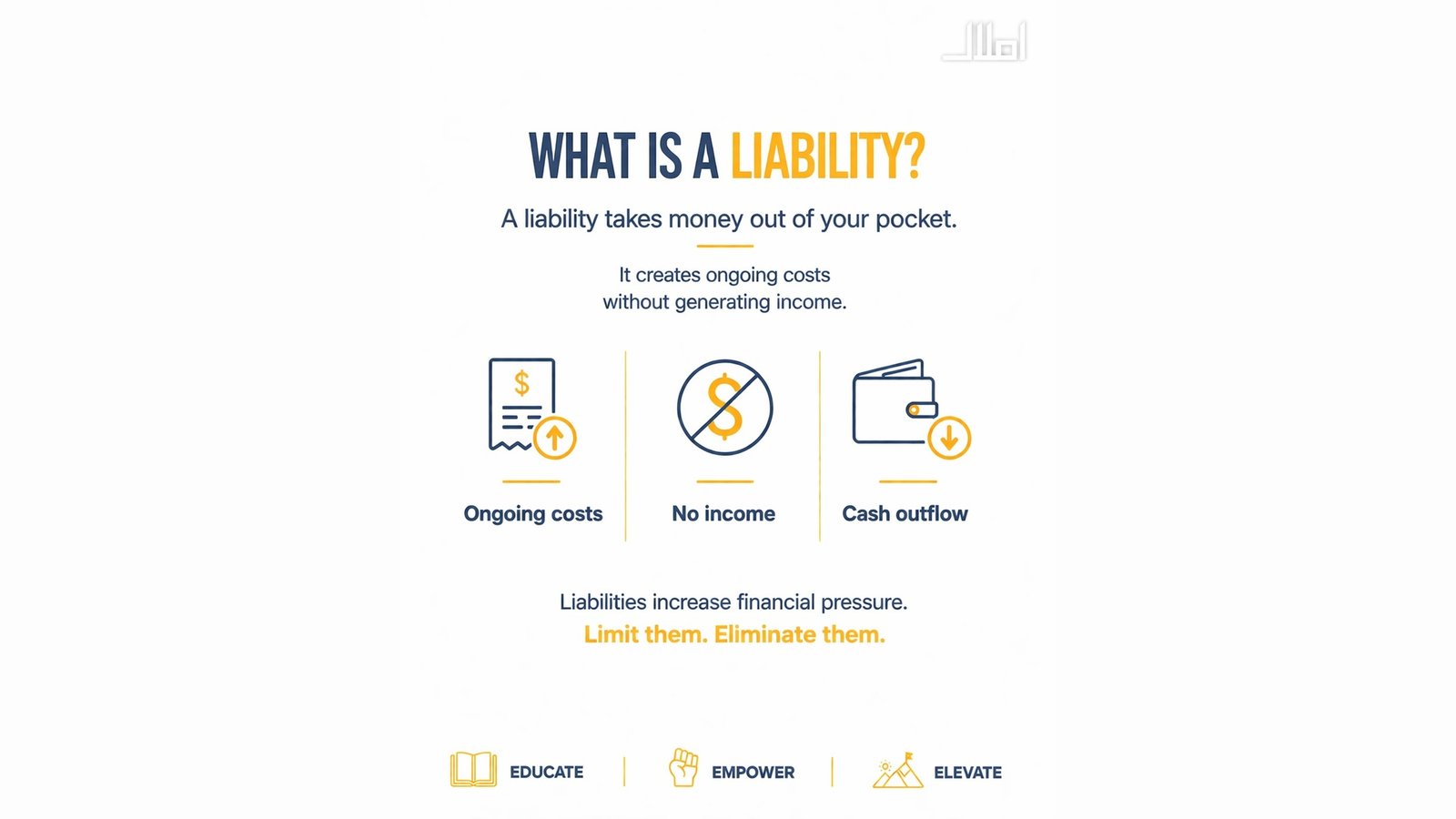

This is where many people get confused. In formal accounting, many items can still be called assets on paper. A personal home, for example, may appear on a balance sheet as an asset. But Kiyosaki’s argument was about financial behavior, not just technical classification. If that home requires mortgage payments, taxes, maintenance, and constant outflows without producing income, then from a cash flow perspective it acts like a liability. Rich Dad’s own articles explicitly make that argument about primary residences.

That is why this lesson is not really about terminology. It is about truth. Not what something is called. But what it does to your monthly financial life. That is the real power of understanding assets vs liabilities.

Why Most People Stay Financially Busy But Never Become Wealthy

A lot of people earn decent money, but they never build real financial freedom. Why? Because they keep increasing liabilities faster than they increase assets. Their salary rises, and so does their lifestyle. Their income grows, and so do their monthly obligations. They buy bigger cars, larger homes, expensive gadgets, and status driven comforts. These things may improve lifestyle, but they usually do not improve financial strength. In many cases, they do the opposite. They require maintenance. They require recurring spending. They require repair and upkeep. They keep pulling active cash out of your pocket.

This is why some people look successful but remain financially under pressure. They own expensive things, but those things are not paying them. And if your possessions depend on your constant labor to survive, then your wealth structure is weak, no matter how impressive it looks from the outside.

“Wealth grows when assets support your life and liabilities stop controlling it.”

Some Things Look Like Assets But Quietly Behave Like Liabilities

This is the trap that catches a large part of the middle class. Many purchases feel like investments, but in reality they drain liquidity, create holding pressure, and delay wealth building. This is where understanding assets vs liabilities becomes critical.

Here are common examples:

1. A personal car

A personal car may be necessary, but it is rarely an income producing asset unless it directly generates business cash flow. Rich Dad’s material uses similar examples, explaining that a vehicle can be a liability for personal use but an asset when it is used in a way that earns money.

2. A self occupied luxury home

A beautiful home may increase comfort and status, but if it is not generating cash flow, it often becomes an expensive financial commitment rather than a productive asset. This is one of Kiyosaki’s most controversial but well known examples.

3. Dead real estate holdings

Some properties rise in value only in theory. They sit idle, generate no monthly income, and may take years to become liquid. During that time, they can tie up capital that could have been producing returns elsewhere.

4. Lifestyle purchases dressed up as achievements

Luxury goods, expensive electronics, prestige spending, and trend driven buying may feel rewarding, but they usually do not create independence. They increase image, not income.

This is why many people stay financially stuck. They are not collecting productive assets. They are collecting financial responsibilities.

What Real Assets Actually Do

A real asset strengthens your position. It either gives you cash flow today or has a strong, realistic path to producing income in the future. Strong assets usually do one or more of the following:

- They put money in your pocket regularly

- They grow in value over time

- They protect purchasing power against inflation

- They reduce dependence on active income

- They help fund the acquisition of more assets

That is how wealthy people keep moving ahead. They do not just save harder. They allocate better. They buy things that keep working even when they are not. Rich Dad’s recent material continues to emphasize building wealth through assets rather than relying only on a paycheck.

This is the real engine of compounding. An asset pays you. That income helps you buy another asset. Then both assets start working together. Over time, your money builds a machine that supports you instead of constantly needing support from you.

Why Cash Flow Is the Real Wealth Builder

Many people obsess over future appreciation. They want something that may become more valuable one day. And yes, appreciation matters. But appreciation alone does not create monthly breathing room unless you sell the asset. Cash flow does. That is why serious investors value income generating assets so highly. Rich Dad’s personal finance material repeatedly ties the asset concept to cash flow rather than only price appreciation.

When an investment pays you monthly, it starts changing your financial life immediately. You become less dependent on your next salary. Less dependent on the next sale. Less dependent on the next deal or commission. Your asset starts sharing the burden. This is where financial freedom begins. Not when you look rich. But when your income sources multiply beyond your own labor.

“Real freedom begins when your income is no longer limited to your effort.”

How Rich People Use Assets to Become Even Richer

The rich often become richer because they stay committed to acquiring productive assets. They do not stop after one. They repeat the cycle. They invest in an asset. The asset generates income. That income is either reinvested or used to acquire the next asset. This is one of the central messages in the Rich Dad ecosystem, which repeatedly teaches readers to audit what generates cash flow and what drains it.

That repeated discipline creates separation over time. One person earns and spends. Another earns and builds. Years later, the difference becomes massive. The wealth gap often widens not because one person worked infinitely harder, but because one kept feeding liabilities while the other kept feeding assets. That is the long term effect of understanding assets vs liabilities and acting on it consistently.

Why Rental Real Estate Is One of the Clearest Examples of a True Asset

Rental real estate, when selected correctly, is one of the most practical examples of an asset because it can combine two major wealth drivers in one structure:

Monthly income

Long term value growth

That is why real estate has remained such an important part of serious portfolio building. A rental property can potentially pay you while also appreciating over time. That combination is powerful because it creates present cash flow and future upside together. This is also why the original IMLAAK article framed rental income as one of the ways wealthy people create easier money through passive income structures. The article presents rental income as a way to create wealth through recurring inflows rather than relying only on active effort.

When rental income is strong, it can help you:

- Cover expenses

- Reduce financial pressure

- Preserve liquidity

- Reinvest in another opportunity

- Create long term monthly support

This is the difference between owning property and owning productive property. Not all real estate is an asset. The right real estate is.

Not Every Property Is an Asset

This is a very important point for investors, especially in markets where people assume every plot, apartment, or file is automatically a smart investment. That is not true. A property only becomes a strong asset when the numbers, demand, usability, and cash flow potential make sense.

A poor investment can still sit under the label of real estate and behave like a liability if it has:

- Weak rental demand

- Poor location logic

- High maintenance burden

- Legal uncertainty

- Bad developer delivery risk

- Low occupancy potential

- Dead capital with no income

That is why real estate investing should never be based on hype alone. It should be based on use case, income logic, security, and long term value. Buying blindly is not investing. It is speculation wearing a suit.

The Middle Class Mistake: Buying for Status Instead of Income

This is one of the biggest financial mistakes people make. They save money for years, then put it into something that makes them look successful rather than something that makes them financially stronger. The result is common and painful. They may own expensive things, but they still feel monthly stress. They may have visible wealth, but not usable cash flow. They may look established, but remain dependent on active work.

That is not real financial freedom.

The wealthy tend to think differently. They ask better questions:

- Will this produce income?

- Will this protect capital?

- Will this hold demand?

- Will this help me acquire another asset?

- Will this improve my position over the next five to ten years?

That is investor thinking. And it is very different from consumer thinking.

Appreciation Is Good. Cash Flow Is Better. Both Together Are Best

The ideal investment is not just something that may rise in value. It is something that can support you while it rises in value. That is what makes income generating real estate so attractive when chosen correctly. A strong rental property may offer:

- Monthly cash flow

- Long term appreciation

- Inflation protection

- Usable real world value

- Exit flexibility

- Portfolio stability

This is why productive real estate often becomes a cornerstone of wealth building. A dead asset may make you wait. A productive asset starts helping you immediately.

Final Thought: Ask the Most Important Question in Investing

Robert Kiyosaki’s enduring lesson is powerful because it forces honesty. Before buying anything, ask: Is this putting money in my pocket, or taking money out of it?

That one question can protect you from years of financial confusion. Many people spend their lives chasing income while slowly building liabilities. The wealthy focus on acquiring assets that generate cash flow, protect capital, and keep compounding over time. That is why they often keep getting richer. They do not just work for money. They keep buying things that pay them.

And among the clearest examples of that principle is well selected rental real estate, because true wealth is not just about ownership. It is about owning income. In the end, the lesson of assets vs liabilities is not theoretical. It is practical, personal, and deeply connected to how wealth is actually built.

FAQ Section

What is the difference between an asset and a liability?

In Robert Kiyosaki’s cash flow based framework, an asset puts money in your pocket, while a liability takes money out of your pocket. This definition focuses on real life financial impact rather than only formal accounting labels.

Is a house an asset or a liability?

It depends on how it functions. A self occupied home may be an asset in accounting terms, but if it creates regular expenses without generating income, Kiyosaki argues it behaves like a liability from a cash flow perspective.

Why do rich people focus so much on cash flow?

Cash flow is important because it makes you less reliant on active income and helps you pay for future investments. Assets that make money can help you live your life, lower your stress, and speed up compounding. Rich Dad’s materials consistently stress building income streams that work independently of a paycheck.

Is all real estate an asset?

No. Real estate only becomes a strong asset when it has sound rental demand, usability, security, and income potential. A poorly selected property can tie up capital and behave more like a liability.

What makes rental income such a great way to build wealth?

Renting out a property can bring in regular cash flow, and the property itself may also go up in value over time. That combination of present income and future upside is one reason rental real estate is often considered a strong wealth building tool. The original IMLAAK article also frames rental income as a path to building wealth through passive income.

What is the biggest mistake average investors make?

One common mistake is buying for image instead of income. Many people buy expensive things that increase monthly outflow instead of buying assets that generate cash flow and improve long term financial strength.This is why serious investors need to know the difference between assets Vs liabilities.

At IMLAAK, we believe serious investing starts with clarity. The goal is not just to buy property. The goal is to buy the right kind of property, one that protects your capital, strengthens your cash flow, and helps you build long term wealth with logic, not emotion.

Shahnawaz Yaqub Bhatti

Investment Consultant and CEO at Imlaak

- Mobile: +92 300 3343336 (WhatsApp)

- Mobile: +92 333 1616160 (WhatsApp)